I have been hearing something a little different during the recent set of Earning calls delivered by CEOs to Wall Street analysts. Right upfront, many executives are warning their shareholders that a little know rule change to the tax code is going to have a potentially huge impact on businesses and business decision-making in 2022 and beyond.

by CEOs to Wall Street analysts. Right upfront, many executives are warning their shareholders that a little know rule change to the tax code is going to have a potentially huge impact on businesses and business decision-making in 2022 and beyond.

If you are a graduate of one of Advantexe’s Business Acumen programs, I am hopeful that you remembered one of the lessons about depreciation and capitalization of R&D and software. Depreciating an asset gives a business a chance to account for the wear and tear of equipment and is treated as an expense on the P&L. You might think that being treated as an expense is a bad thing, but since most companies have already paid cash for the asset in a previous time period, the ability to take depreciation as an expense is a good thing. Because it reduces net income! Wait, why is reducing net income a good thing? Well, when you reduce net income, you are reducing your tax obligation! Remember, one of the key metrics of success other than profit is your net cash flow and by reducing your tax obligation (and paying less in taxes) you are actually increasing your net cash flow.

The same sort of concept has applied to certain investments in R&D. Many companies have capitalized their R&D expense, as an incentive from the government to invest more in R&D which creates more innovation and jobs, and as a way to reduce their tax obligation. Up until now, these R&D expenses could be taken in the year they were incurred which reduced profit, which reduced the tax obligation.

Big Changes

But a big change is here for companies that expense R&D costs as incurred. Those expenses may no longer be eligible for an immediate deduction unless Congress changes the rules by the end of 2022.

As of today, the current law requires companies to capitalize all of their R&D costs, including software development costs, incurred in tax years beginning after December 31, 2021. This means that beginning in 2022, your company would no longer be permitted to deduct R&D expenses in the year they were incurred. Instead, you would be required to amortize those expenses over 5 years if you are conducting the R&D in the USA or 15 years outside of the USA.

This new law will significantly impact pharmaceutical companies and technology companies because they spend a lot of money on R&D. A typical pharmaceutical company spends about 25% of their revenue on a common size analysis basis on R&D while other industries like retail may spend less than 1% on R&D.

Example: Innovex Pharmaceuticals

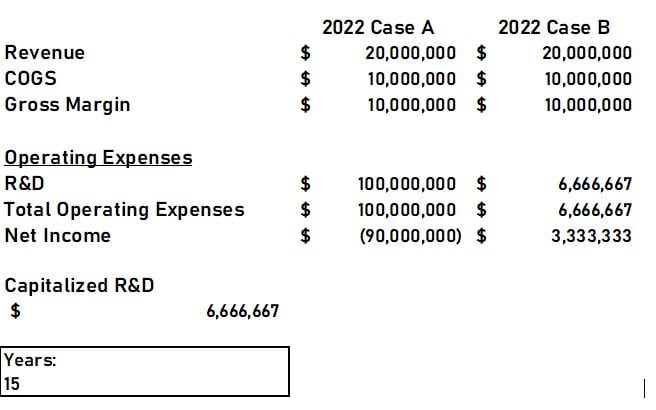

Imagine Innovex (the name of one of our fictional business simulation companies) has $10 million in revenues and spends $100 million offshore on drug development. Traditionally, the company would have a $90 million taxable loss. When the new law goes into effect, however, the company would have a $3.4 million taxable profit instead. So not only did they lose money, but they are also paying taxes as well!

Let’s look at the math:

We present Case A and Case B. In Case B, the total R&D expense is divided by 15 which is the number of years that the R&D must be capitalized if it’s outside of the USA.

The Impact

By now, you may have realized the real impact of this new tax rule. If a company like Innovex in this example has to pay taxes on their net income even though they “really” lost $90 million that means, not only are they losing tax credits for their loss (which could be in the millions of dollars), they are spending money paying on taxes that could be spent on more R&D or even some pre-launch Marketing.

What it Could Mean to Your Everyday Decision Making

Consider this quote from the CEO of a large global company in the defense industry when talking about the guidance of free cash flow for 2022:

“Our free cash flow guide of $2.15 billion to $2.25 billion incorporates current tax regulations which require us to capitalize R&D expenditures beginning in 2022 versus the prior practice of annual deductions resulting in tax payment increases.”

In this case, the free cash flow projection for next year is about $500,000 less

Summary

Without a doubt, these new tax rules will impact your everyday decision-making. Budgets will be a little tighter and there will be a significant amount of pressure on you to make the best decisions possible because there simply is less cash. Knowing this, if you are able to use your business acumen skills to make a better business case, you have a better chance of getting the resources you need.